Direct answer

How much does income protection cost in Australia?

Income protection in Australia typically costs between $30 and $450+ per month. The exact amount depends on your age, occupation, cover amount, smoking status, waiting and benefit periods, and policy type.

Income protection replaces part of your income if you're unable to work due to illness or injury. Premiums are often tax-deductible when held outside super.

Based on clerical worker: $6,000 monthly benefit, 2-year benefit period, 2-month waiting period.

Pricing table

Average income protection premiums by age, gender and smoking status

Age and smoking status are the two biggest drivers of cost. Premiums roughly quadruple between your 20s and late 50s, and smokers pay 30–50% more at the same age.

| Age band | Male non-smoker | Male smoker | Female non-smoker | Female smoker |

|---|---|---|---|---|

| 25-29 | $30 | $42 | $42 | $59 |

| 30-34 | $31 | $43 | $44 | $60 |

| 35-39 | $33 | $46 | $46 | $65 |

| 40-44 | $36 | $51 | $51 | $73 |

| 45-49 | $48 | $68 | $69 | $98 |

| 50-54 | $79 | $111 | $114 | $162 |

| 55-59 | $131 | $186 | $185 | $263 |

Example pricing: clerical worker, $6,000 monthly benefit, 2-year benefit period, 2-month waiting period.

Cost factors

What changes income protection costs?

Six factors determine your premium. Age and occupation have the biggest impact — but benefit and waiting periods can shift the number materially without changing your cover.

- Age

- Older = higher cost. Premiums rise sharply from age 45.

- Smoking

- Adds 30–50% for income protection, depending on product and age.

- Gender

- Females pay more for income protection than males at the same age.

- Occupation

- Riskier roles increase income protection costs — occupation class drives price more than employment type.

- Premium type

- Variable Age-Stepped vs Variable changes your long-term total cost significantly.

- Benefit & waiting period

- Longer benefit periods or shorter waiting periods both increase your premium.

Special case

Self-employed workers

Costs are not necessarily higher for self-employed workers — for many office-based occupations, there is no price difference at all. In higher-risk or more physical occupations, premiums can be higher, generally due to the higher likelihood of a claim and the absence of safety nets like sick leave or employer-provided cover.

Besides price, self-employed people face different considerations when buying income protection — primarily in how income is assessed and what circumstances can cause benefit payments to be reduced or adjusted. See our guide on income protection for self-employed Australians for the detail.

Premium structures

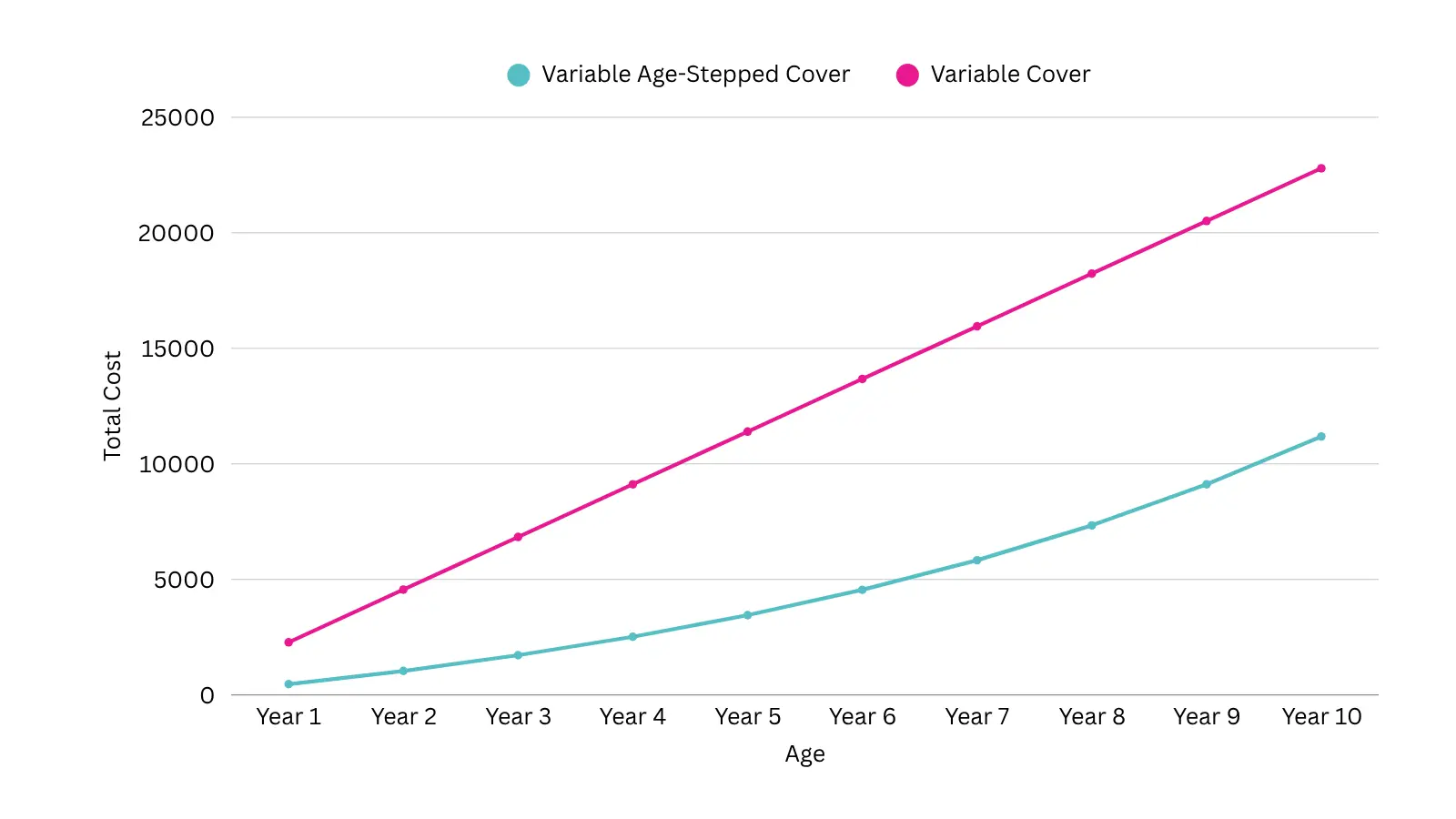

Variable age stepped vs variable premiums — which is cheaper?

When choosing income protection cover, you'll need to decide between Variable Age-Stepped and Variable premiums. The naming isn't helpful, but the difference matters.

Variable age stepped

Starts cheaper, increases each year

Starts cheaper, but increases each year as you age. Best if you plan to hold the policy for fewer than 10 years.

Variable

Starts higher, stays largely the same

Starts higher, but stays largely the same. Can still increase with CPI or insurer-wide repricing — but won't increase simply because you've turned another year older.

Tip: if you plan to keep your policy more than 10 years, variable (level) premiums are usually more cost-effective overall. The chart below shows the cumulative cost difference based on our analysis.

Risk factor

Why smoking impacts income protection costs

Smoking is a major health risk — and insurers price that risk in.

30–50%

more for income protection

The exact loading depends on your age, occupation and insurer.

Non-smoker reassessment

If you've been smoke-free for 12 months, many insurers will reclassify you as a non-smoker — unlocking significant premium savings. Worth requesting a reassessment once you reach this milestone.

Insurer comparison

Why comparing income protection policies can save you thousands

Income protection prices vary massively between insurers. For the same person and the same cover, we've found an average 50% premium difference between the cheapest and most expensive providers.

~50%

Real-world price gap

Average difference between the cheapest and most expensive insurers for the same cover on the same person.

That's why it's critical to compare quotes — not just for the lowest price, but for the best value in terms of cover, exclusions, and claims experience.

Compare income protection quotes See real prices from leading insurers in minutes.

Other types of cover

Income protection is one part of protecting your income and family. Compare costs across the other cover types.

Frequently Asked Questions

How much does income protection insurance cost per month in Australia?

Average premiums range from $30/month in your 20s to $450+/month in your late 50s, depending on cover settings and lifestyle factors.

Why do income protection premiums increase with age?

Older age equals higher risk of illness or death — insurers price in this increased risk.

What affects income protection premiums?

Occupation, benefit period, waiting period, age, and smoking status all impact cost. Higher risk or more generous terms mean higher premiums.

Does income protection cost more if I'm self-employed?

Not necessarily. For many office-based self-employed occupations, premiums are the same as for employed workers in the equivalent role — your occupation class drives the price more than your employment type. In higher-risk or more physically demanding occupations, premiums tend to be higher: the likelihood of a claim is greater, and self-employed workers don't have employer sick leave or workers' compensation to fall back on. The bigger differences for many self-employed workers is in how income is assessed for cover and how benefits are calculated at claim time — see our guide on income protection for self-employed Australians for the detail.

Are premiums tax-deductible?

Income protection premiums are often tax-deductible in Australia, depending on how the policy is structured. You should confirm eligibility with a tax professional.

Is variable age stepped or variable cover cheaper?

Variable age stepped is cheaper short-term; variable cover can win long-term if you hold the policy over 10+ years.

Do all insurers charge the same for income protection?

No — some can be 50% more expensive for the same cover. It's always worth comparing.

Why do smokers pay more?

Smoking significantly increases health risks, doubling life insurance costs and increasing income protection premiums by 30–50%.

Can I get reclassified as a non-smoker?

Yes. After 12 months without smoking, many insurers will reclassify you as a non-smoker, reducing your premiums.