How Much Does Life Insurance Cost in Australia? (2026)

Most Australians pay between $25-$300+ per month

Your exact price depends on age, smoking status, cover level and how you buy.

See your real life insurance cost instantly - no contact details required.

Get your personalised estimate

Cheapest Life Insurance Premiums in Australia (2026)

Most Australians pay between $25-$300+ per month, with some policies starting from around $17-$18/month for younger, low-risk applicants.

Here are example monthly premiums from leading insurers:

Based on sample profiles for 25, male, non-smokers with $500,000 cover.

- Zurich - from $17/month

- OnePath - from $18/month

- Acenda - from $23/month

- Encompass - from $23/month

- Neos - from $26/month

With Keep Insurance, eligible policies can include up to 12.5% cashback each year - reducing the real cost of your cover over time.

When you're asking "How much does life insurance cost in Australia?" the answer can be hard to find! Premiums vary widely depending on a number of factors - including your age, health, occupation, how you buy your policy and more, so the answer is often the unhelpful “it depends.”

That's why we've built this premium guide - to show real numbers, factors that affect your pricing, and tools to help you compare quickly.

Not sure which type of cover you need? See our guide to comparing life insurance types in Australia .

📊 Average Life Insurance Costs in Australia (2026)

Most Australians pay between $25-$300+ per month depending on age, gender and smoking status. Premiums increase significantly with age, and smokers can pay up to twice as much as non-smokers.

Use the calculator above to see how your pricing compares.

| Age Band | Male Non-Smoker | Male Smoker | Female Non-Smoker | Female Smoker |

|---|---|---|---|---|

| 25-29 | $26 | $46 | $18 | $35 |

| 30-34 | $22 | $43 | $17 | $33 |

| 35-39 | $21 | $48 | $17 | $35 |

| 40-44 | $24 | $64 | $19 | $45 |

| 45-49 | $36 | $102 | $29 | $68 |

| 50-54 | $67 | $176 | $52 | $113 |

| 55-59 | $205 | $322 | $103 | $205 |

Example pricing: $500,000 cover, clerical occupation, stepped premiums. As at 1 January 2026.

Based on real insurer pricing analysis across multiple providers in Australia.

What this means for you:Life insurance is generally cheapest when you're younger and increases significantly with age. Locking in cover earlier when you are healthy can help reduce long-term costs.

🧠 What Changes Life Cover Costs?

| Factor | Impact on Premiums |

|---|---|

| 🕒 Age | Older = higher cost |

| 🚬 Smoking | Adds 30-100% depending on product |

| 🚻 Gender | Males pay more for Life; females for Income Protection |

| 📊 Premium Type | Variable vs Age-Stepped changes long-term costs |

| ❤️ Health | Insurers can apply premium loadings or exclusions based on your health and medical history. |

| 🏢 Insurer | Almost identical policies from different insurers can vary by over 50% |

| 🛒 How you buy | Some advisers will charge a fee as well as commisson. Some companies can give effective discounts of 10% or more as cashbacks or rebates - it's worth shopping around. |

🏷️ Compare Life Insurance Providers - Prices Can Vary by 50%

Life insurance prices can vary significantly between insurers. For the same person and cover, premiums can differ by 50% or more depending on pricing models, underwriting and policy structure. In fact a recent review found that one insurer was 96% more expensive for a TPD policy at age 55.

By comparing quotes across insurers, you can often pay significantly less for essentially the same cover - and in some cases, access cashback or commission rebate structures that reduce what you pay over time.

Compare Life Insurance QuotesSee real prices and potential savings in minutes

How You Buy Life Insurance Matters

The way you buy life insurance can significantly impact price, features and the level of support you receive.

Through super

Often one of the cheapest ways to get cover, but not always. Cover levels and features can be limited, and flexibility is reduced compared to retail policies.

Direct (over the phone)

Convenient to set up, but typically more expensive. Research shows direct policies can cost 50% more, and in some cases up to 4× more than comparable retail cover.

Is direct insurance worth the cost?Financial adviser

Personal advice can be valuable, especially for complex needs. However, this can include advice fees as well as commissions on top.

Insurance broker

Brokers can help compare products and pricing, but don't provide personal advice. Some may have limited insurer panels or retain full commissions.

Tip: Look for brokers that offer rebates or cashback options.

How to Reduce Life Insurance Costs

If your premiums feel high, there are several ways to reduce what you pay - often without changing your cover:

- Compare insurers - prices for the same cover can vary by 50% or more

- Adjust your cover amount to better match your needs

- Review policy settings like waiting and benefit periods

- Improve your health or smoking status over time

- Access cashback or commission rebate structures that can return part of your premiums over time

In many cases, the biggest savings come from simply comparing providers and choosing a better-structured policy. Learn more about reducing premiums.

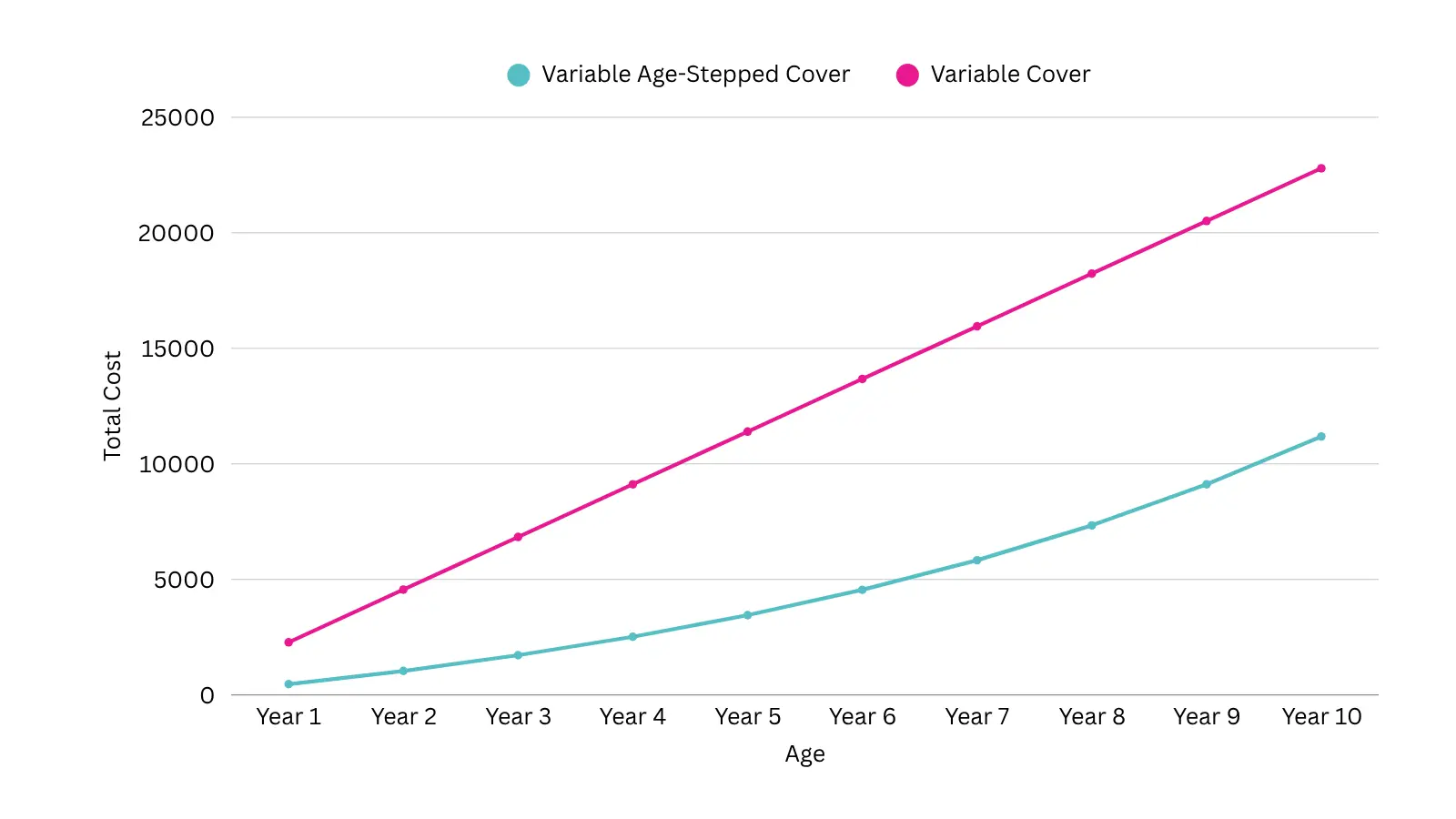

🔁 Variable Age-Stepped vs Variable Premiums (Stepped vs Level) - Which Costs Less Long Term?

Short answer: Age-stepped premiums are cheaper at first, but variable (level) premiums are usually cheaper if you keep your policy long term.

- ➤Variable Age-Stepped: Starts cheaper, but increases each year as you age

- ➤Variable Premiums: Start higher, but stay more stable over time (may increase with CPI, or if the insurer changes the price for all policies - ie won't increase just because you are one year older)

If you plan to keep your cover for more than 10 years, variable premiums are often more cost-effective overall.

Learn more about Variable Age-Stepped and Variable premiums

🚭 Why Smoking Impacts Life Insurance Costs

Smoking can significantly increase what you pay for life insurance - in many cases, doubling your premiums.

- 💸Up to 100% more for life insurance

- 💸30-50% more for income protection

The exact impact depends on your age, cover and insurer - use the calculator above to see your pricing.

If you've been smoke-free for 12 months, many insurers will reclassify you as a non-smoker - which can significantly reduce your premiums.

Life insurance is just one part of protecting your income and family. If you're also comparing costs for cover that replaces your salary, see our guide to Income Protection costs in Australia .

Frequently Asked Questions

How much does life insurance cost in Australia? +

Life insurance in Australia typically costs between $25 and $300+ per month, depending on your age, cover amount, health, and smoking status.

How much does $500,000 of life insurance cost per month? +

For a non-smoker, $500,000 of cover typically costs $18-$50 per month in your 20s and $50-$300+ per month in your 50s. Costs increase with age and health risk.

How much does $1 million of life insurance cost per month? +

For a non-smoker, $1 million of cover typically costs $35-$80 per month in your 20s and $200-$450+ per month in your 50s, depending on health and smoking status.

What factors affect life insurance costs in Australia? +

Life insurance premiums are based on age, smoking status, health, occupation, lifestyle, and the amount of cover selected.

Why do premiums increase with age? +

As you get older, the risk of illness and death increases. Insurers adjust premiums accordingly, especially for stepped policies that rise each year.

Do all insurers charge the same? +

No. Premiums for the same cover can vary by 50% or more between insurers, which is why comparing quotes is important.

Is life insurance expensive in Australia? +

Life insurance can be relatively affordable when you're younger, with premiums often starting from around $20-$30 per month. Costs increase significantly with age and risk factors.

Show more questions

Can I reduce my life insurance premiums? +

Yes. You can reduce premiums by comparing insurers, adjusting your cover amount, improving your health, or reviewing your policy regularly.

Is stepped or level life insurance cheaper? +

Stepped premiums are cheaper initially but increase each year. Level premiums start higher but can be more cost-effective if you keep your policy long term.

Why do smokers pay more for life insurance? +

Smoking significantly increases health risks, which leads insurers to charge higher premiums-often up to double compared to non-smokers.

Can life insurance premiums be reduced without changing cover? +

Yes. In some cases, cashback or commission rebate arrangements can return part of your premiums over time, reducing the overall cost without changing your cover.

Can I get money back from life insurance premiums? +

Some providers allow you to receive a portion of your premiums back over time through cashback or commission rebate arrangements, reducing the overall cost of your cover.

✅ Summary: Key takeaways for 2026

- Smokers pay up to double the premium.

- Life insurance gets expensive from age 45+.

- Stepped vs. level premiums impact long-term pricing.

- Comparing insurers can cut your costs by 50%.