General Knowledge

On this page

Two surprising things jumped out when I reviewed the APRA claims statistics: around one in four claimants for TPD and DII claims raise a dispute, and the rate varies materially depending on who the claim is with.

When APRA and ASIC present their headline results, they focus on claim admission rates: the proportion of finalised claims that are accepted and paid. On this measure, most insurers cluster within a few percentage points of each other. At the end of the day, this is arguably what matters most: if you submit a claim, what is the likelihood of it being accepted?

Claim acceptance

Admitted Claims

| Insurer | Death | TPD | Trauma | DII |

|---|---|---|---|---|

| AIAA | 95.6% | 76.0% | 85.9% | 93.8% |

| ClearView | - | 57.7% | 84.8% | 90.3% |

| MetLife | - | - | 87.7% | 84.6% |

| Acenda Life | 97.6% | 84.9% | 89.6% | 95.4% |

| NobleOak | - | - | 99.2% | 98.0% |

| RLA | 98.6% | 87.5% | 86.1% | 96.3% |

| TAL | 97.2% | 79.8% | 88.6% | 93.2% |

| Zurich | 96.4% | 85.8% | 86.4% | 95.8% |

| Total | 97.0% | 82.3% | 87.6% | 94.3% |

Admitted Claims % = Admitted Claims / Finalised Claims.

DII means disability income insurance, which is better known in Australia as income protection insurance. AIAA refers to AIA, NobleOak includes Neos and Encompass, and RLA refers to Resolution Life.

But what admission rates do not show is whether a claimant had to fight for that outcome, or whether the insurer was able to accept and process it without a dispute ever arising.

Cover type comparison

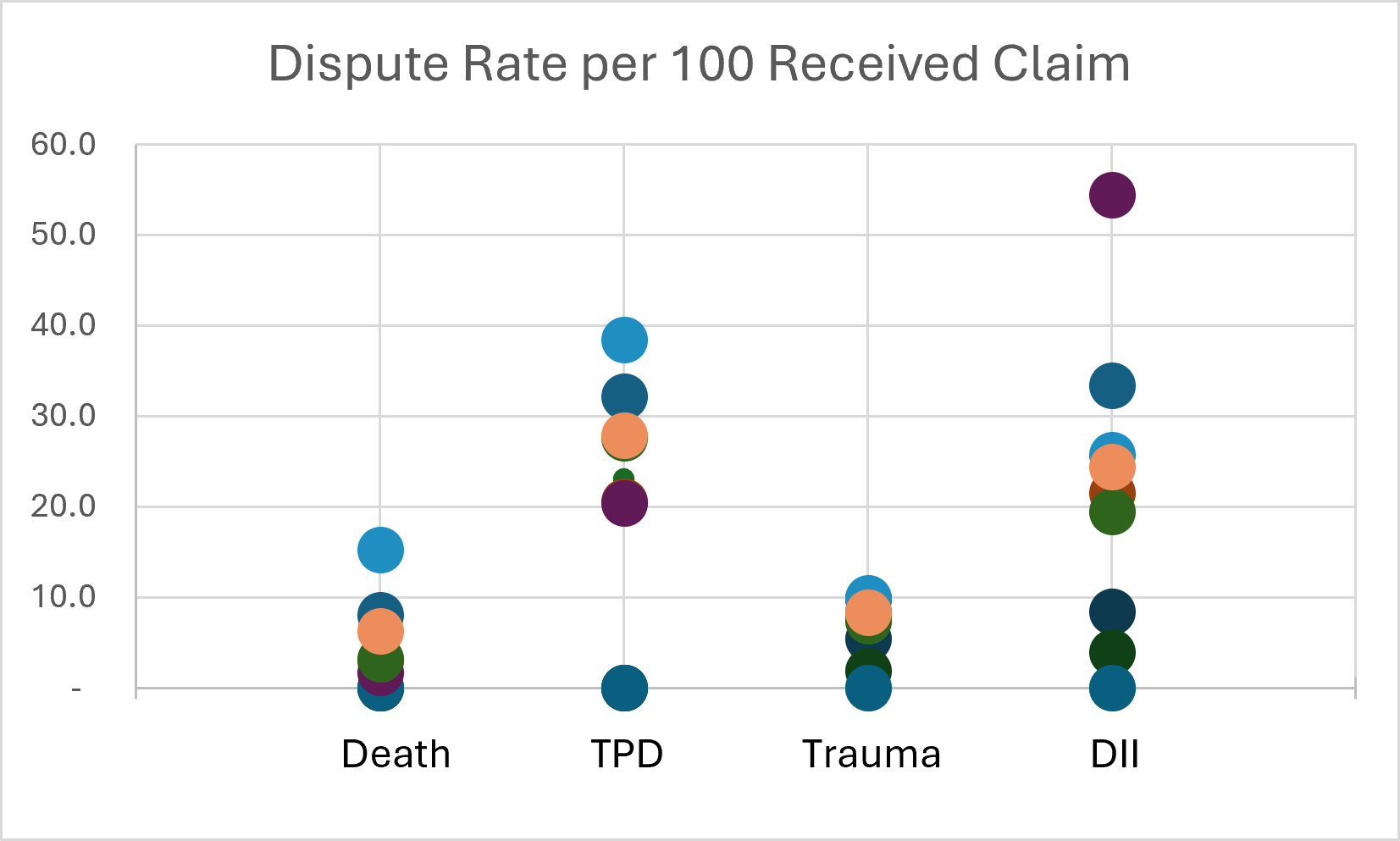

Dispute rates vary considerably by cover type

The chance of a dispute varies considerably between cover types at the market level. The difference is stark, but perhaps explainable.

Death claims

6.3%

dispute rate

Trauma claims

8.3%

dispute rate

TPD claims

27.9%

dispute rate

IP / DII claims

24.4%

dispute rate

Dispute rate = disputes lodged / claims received.

Death and trauma claim definitions are relatively objective: a death is a death; a listed medical event either occurred or it did not. Disability definitions are a different matter. TPD policies typically require a claimant to demonstrate they are unable to ever return to work, a threshold that depends heavily on medical evidence, the insurer's interpretation of policy wording, and how occupation and capacity are assessed.

Income protection goes a step further. Ongoing claims require continuous review, creating repeated touchpoints where disputes can emerge. A claimant's condition may improve, deteriorate or shift in ways that are open to interpretation.

Insurer variation

Variation between insurers

Where things get harder to understand is the variation between insurers.

Some variation is inevitable and would be impacted by each insurer's product definitions and processes. This could explain the extent of variations seen for death, TPD and trauma, but it is harder to understand what is driving the differences in DII.

The table below shows the spread of dispute rates across insurers for each cover type. The DII column is particularly striking.

| Insurer | Death | TPD | Trauma | IP / DII |

|---|---|---|---|---|

| AIAA | 8.1 | 32.2 | 8.4 | 33.4 |

| ClearView | - | 23.1 | 9.1 | 9.8 |

| MetLife | - | - | 5.5 | 8.5 |

| Acenda Life | 3.0 | 20.6 | 7.6 | 21.5 |

| NobleOak | - | - | 1.9 | 3.9 |

| RLA | 1.7 | 20.5 | 9.8 | 54.5 |

| TAL | 3.2 | 27.6 | 7.4 | 19.5 |

| Zurich | 15.2 | 38.5 | 9.9 | 25.8 |

| Total | 6.3 | 27.9 | 8.3 | 24.4 |

Figures = 100 x Disputes Lodged / Claims Received.

DII means disability income insurance, which is better known in Australia as income protection insurance. AIAA refers to AIA, NobleOak includes Neos and Encompass, and RLA refers to Resolution Life.

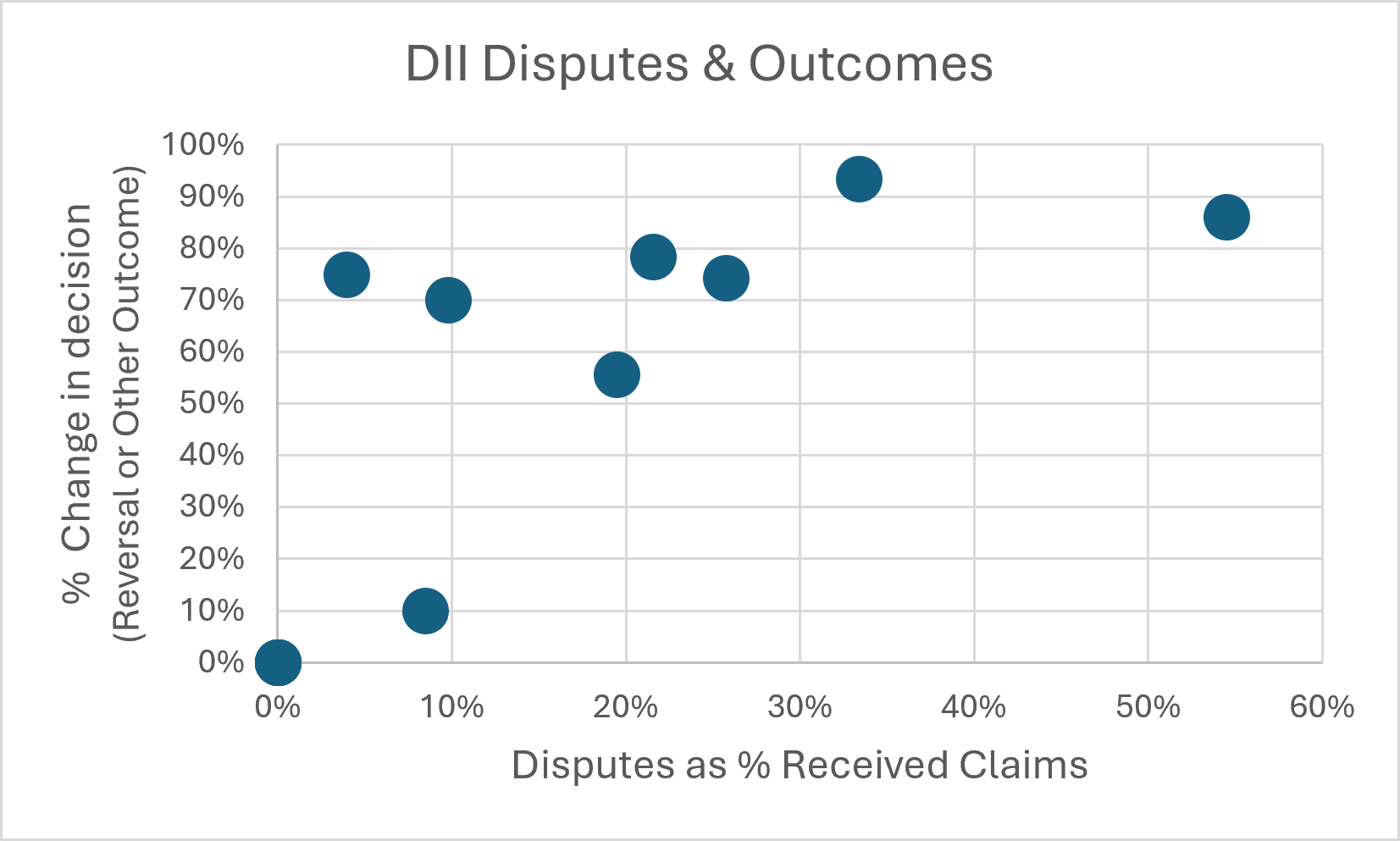

Dispute outcomes

What happens after a DII dispute?

This variation did not make sense in the context of similar admission rates until I dug a little deeper and found a correlation between high dispute rates and the likelihood of the original decision being changed as a result of the dispute, either through the original decision being reversed or another dispute outcome.

| Insurer | Disputes per claim | Disputes resulting in a change |

|---|---|---|

| AIAA | 33% | 94% |

| ClearView | 10% | 70% |

| MetLife | 8% | 10% |

| Acenda Life | 22% | 78% |

| NobleOak | 4% | 75% |

| RLA | 54% | 86% |

| TAL | 19% | 56% |

| Zurich | 26% | 74% |

Disputes per claim = Disputes Lodged / Claims Received. Disputes with change = (Decisions Reversed + Other Dispute Outcomes) / Disputes Resolved.

DII means disability income insurance, which is better known in Australia as income protection insurance. AIAA refers to AIA, NobleOak includes Neos and Encompass, and RLA refers to Resolution Life.

This correlation makes sense. If poor claims decisions are being made in the first place, they are more likely to be disputed, which in turn results in those decisions being reversed or adjusted. It perhaps suggests the issue may be less about the complexity of the claim and more about the quality of the initial assessment.

That correlation is also required for the percentage of claims admitted to be relatively consistent between insurers. If one insurer has many more disputes, but a high proportion of those disputes lead to changed outcomes, the final admitted claims percentage can end up looking similar to competitors even though the claimant experience was very different.

Claimant view

A claimant's takeaway

Headline admission rates are important, but they are not the whole story. For a claimant, the difference between a smooth acceptance and a disputed claim can mean months of uncertainty, repeated medical evidence requests and financial pressure at exactly the wrong time.

I would love to hear from others who have insights into what may be driving these differences, particularly for DII claims.

Frequently Asked Questions

What does APRA mean by admitted claims?

In this article, admitted claims refers to admitted claims divided by finalised claims. It indicates the proportion of finalised claims that were accepted and paid.

Why are TPD and DII dispute rates higher?

TPD and DII claims rely heavily on disability definitions, medical evidence, occupation, capacity and ongoing assessment. These judgement-based elements create more room for disagreement than many death or trauma claims.

Does a high admission rate mean the claim process is easy?

Not necessarily. A claim can ultimately be admitted after a dispute, reversal or adjusted outcome. Admission rates do not show how much friction a claimant experienced before payment.

What stood out most in the DII data?

The striking point was the relationship between higher DII dispute rates and a higher share of disputes resulting in changed outcomes, suggesting initial assessment quality may be an important factor.

Compare quotes and start saving

Real-time quotes from leading Australian insurers in five minutes — no email required.